Access to housing in Spain: rising pressure and the importance of clear data

Accessing housing has become increasingly challenging across many countries. Real estate markets are under strain due to sustained price increases, limited affordable supply and demographic and economic changes that affect both renting and homeownership.

In Spain, demand for housing continues to grow, particularly for rental and affordable options, while supply remains constrained. This imbalance is further shaped by an evolving regulatory environment, with new laws and public programmes designed to improve access through financial support, rehabilitation grants and rental incentives.

These measures can be effective, but their impact depends on proper execution. Eligibility criteria, technical documentation, property valuation and energy certification often determine whether support can be accessed.

At Accumin, we see data as the starting point for better decisions. We continuously analyse residential market dynamics, focusing on price evolution, regulatory context and affordability indicators, with the aim of providing a rigorous and accessible perspective on housing access.

To assess the current pressure in Spain, we analysed the latest IMIE Local Markets report, produced by Tinsa España and Accumin Intelligence. The report combines price trends based on Tinsa’s valuation data with financial and market activity indicators.

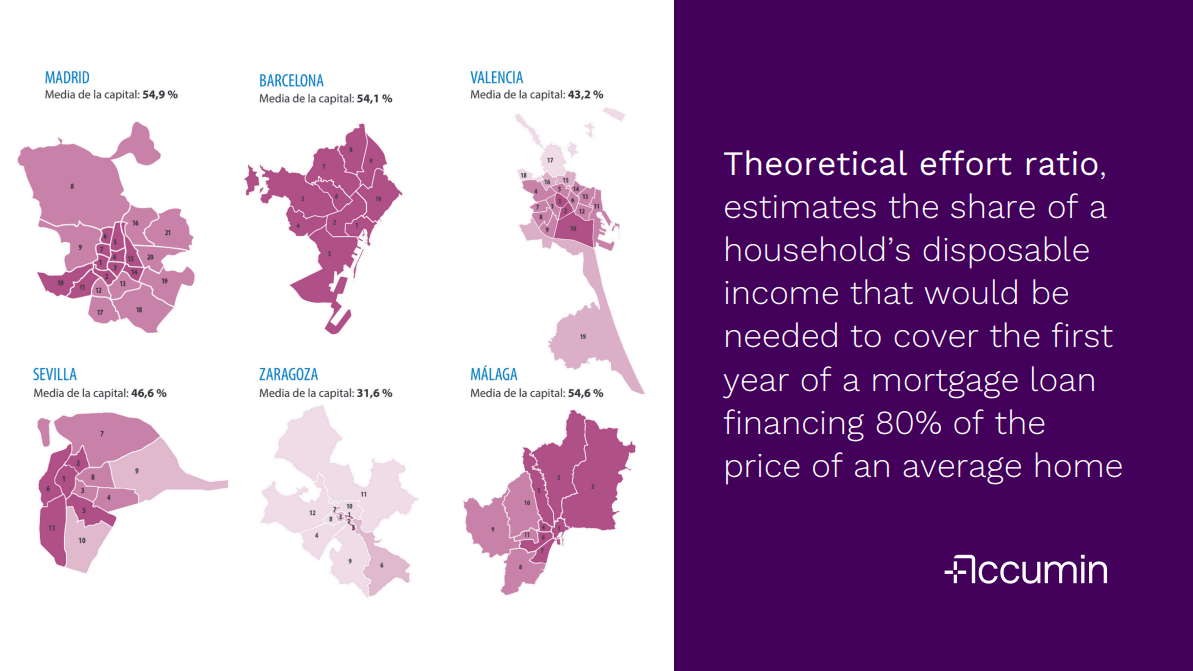

A key metric in the analysis is the theoretical effort ratio, which estimates the share of household disposable income required to cover the first year of a mortgage financing 80% of the average home price. The national average stands at 34.1%, while seven provinces exceed the 35% threshold often considered a reasonable upper limit. The highest levels of pressure are observed in Málaga (58%), the Balearic Islands (49%) and Madrid (45%), followed by Cádiz, Alicante, Sevilla and Barcelona.

At city level, Madrid, Málaga, Barcelona, Cádiz and San Sebastián all exceed 50%, indicating particularly high stress. Values between 40% and 50% are recorded in Sevilla, Granada, Salamanca, Valencia, Palma, Santander and Pamplona. Among Spain’s six largest cities, only Zaragoza remains below the risk threshold, at 32%.

Through our ongoing work, we will continue to monitor these indicators as part of a broader content series analysing access to housing across different markets. After Germany and Spain, the next focus will be Portugal.